Many are asking whether employers are within their rights to take such actions.

“The technology is owned by the government so, in other words, handheld devices, smartphones, because they own it, they can do what they want in terms of how the device is used,” says Daniel Tsai, lecturer on law and technology at the University of Toronto and Toronto Metropolitan University (TMU).

“Me hearing that [governments are] banning TikTok on government phones, that doesn’t raise any alarms; to me, it sounds reasonable.”

Employer ban

Should other employers, particularly those in the private sector, consider this kind of ban? There are some laws that must be accounted for, according to Savvas Daginis, associate business law at Siskinds Law Firm.

When thinking about how much protection needs to be offered, it is the type of data that matters most, he says.

“If you’re just holding onto somebody’s name and maybe address, and let’s say that name and address are in a phonebook that is readily available to everyone, you won’t need to implement incredibly detailed security measures. Whereas maybe you’d have to implement such measures if you had medical data.”

When it comes to protecting data that might be found on, or be available via a company-issued phone, there are several considerations employers should undertake to keep everything safe, says Liam Ledgerwood, associate labour and employment law also at Siskinds Law Firm.

“Each individual employer will likely set out what their expectations are about the extent to which employees need to safeguard confidential and proprietary information and that will generally be dictated by contract — or by an employer policy, about what employees must do,” says Ledgerwood.

The White House endorsed a bipartisan bill that could give the president authority to ban or force a sale of TikTok, support that could hasten passage and break a deadlock over how to address privacy concerns around the popular app.

The bill introduced recently would give the president the ability to force the sale of foreign-owned technologies, applications, software or e-commerce platforms if they present a national security threat to Americans.

It doesn’t mention Beijing-based Bytedance’s TikTok by name, but the video-sharing app, which has about 100 million users in the U.S., is the clear target.

This is the first time the Biden administration has weighed in on legislation to deal with the app, which the White House says pose national security risks. Critics of TikTok say it allows the Chinese government access to data and viewing trends of the roughly 100 million Americans — as well as users globally — who have made it one of the world’s most popular apps.

Ransomware, backdoor exploits and phishing are terms that IT professionals have come to know well.

So, how can employers better prepare for the onslaught? It starts with understanding the “enemy,” knowing your organization’s weaknesses and seeing cyber attacks as a business risk — not just an IT problem, say the experts.

Apart from the stereotypical hooded individual who might wish to cause harm, there are two main threats to be aware of for businesses, according to Adil Palsetia, partner in cyber security at KPMG.

“On one end, you have nation states. Some of those are adversarial to ours and they’re attacking infrastructure, organizations, our IP infrastructure, our connection infrastructure, the communications infrastructure, as well as our financial and banking infrastructure.

As well, there are organized criminals with a simple goal, he says. “Their mandate is crime usually, a means to make more money, and so they’re the ones that we’re hearing about around this uptick in ransomware attacks.”

New ways to exploit organizations are often being rewarded in the criminal underworld, according to Evan O’Regan, associate partner, digital trust and IAM, at IBM.

“Whereas if our credit card number will fetch maybe $10 on the dark web, the identity information can fetch a much higher price on the dark web because those can be used to create synthetic identities to perpetrate more sophisticated fraud and even more. So if I develop an exploit, a backdoor into a company, I can sell that exploit on the dark web multiple times at $10,000 a pop.”

Leaders from Aviva, Ageas, Beazley, Covéa, Kennedys, Just Group plc, Phoenix Group, QBE Insurance, Swiss Re, Zurich Insurance, UnderwriteMe, all supported by the ABI, BIBA and the Chartered Insurance Institute (CII) , have pledged to join the campaign and have committed to leading the way whilst journeying with GAIN to explore paths to neuroinclusion. This, in turn, is hoped to help unlock the potential of neurodivergent individuals within their own lines of business.

Industry leaders on neuroinclusivity

ABI policy adviser for diversity, equity, and inclusion Liisa Antola said that the industry must broaden its collective understanding of what diversity of talent means to accomplish its mission of becoming the most diverse, equitable, and inclusive sector of the UK economy.

“It is our responsibility to ensure everyone can realise their potential and that the workplace provides a supportive environment for neurodivergent individuals,” she said. “That is why we are proud to support organizations like GAIN that pave the way for awareness and neuroinclusion in the insurance and long-term savings sector.”

Ageas head of inclusion Emma Francis praised her company for being an inclusive workplace, saying that it is one in which their people can feel value for their contributions and are able to perform to their fullest regardless of their background, identity, or circumstances.

“We are delighted to be working with GAIN to increase our knowledge, understanding and awareness of neurodiversity in the workplace and how we can continue to improve how we support our neurodivergent colleagues. As well as supporting the fantastic work they are doing to raise awareness of the insurance sector being a neuroinclusive place to work,” Francis said.

Aviva managing director of personal lines Owen Morris said that the company is happy to support GAIN and its campaign to ensure that everyone can reach their full potential in a positive and supportive environment.

“The UK insurance industry can be a wonderful place for talented neurodivergent individuals to work, with so many problems to solve and different ways to think – which will benefit our customers,” Morris said.

Beazley head of social impact Chelsey Sprong noted that diversity of thought is key to the company’s success, and that it is working to ensure that neurodivergent people are empowered and developed in the firm.

“Neuroinclusion and building an understanding of what this means and what more we can be doing to be more neuroinclusive is a priority for us,” she said. “We are also excited to be supporting GAIN in recognising Neurodiversity Celebration Week, and World Autism Acceptance Week.”

CII equality, diversity, and inclusion manager Vivine Cameron said that the professional body is committed to driving equality of opportunity for all regardless of their race, age, gender reassignment, marriage/civil partnership, pregnancy and maternity, sex and sexual orientation, religion or belief, and disability, whether it’s seen or unseen.

“Additionally, the CII seek to be supportive of those experiencing challenges through building resilience, supporting development, and ensuring wellbeing,” Cameron said. “We want all our members, employees, and other stakeholders to feel included, with a positive sense of belonging, so that everyone can add value and fulfil their full potential in the profession.”

Covéa Insurance accessibility for all lead Michelle Neary expressed the firm’s happiness in partnering with GAIN, which is committed to challenging stereotypes about neurological differences.

“Our accessibility for all groups at Covéa aims to ensure that as a business we are fully inclusive, acknowledging and recognising the many talents and advantages of being neurodivergent through recruitment, development and progression,” Neary said. “To support our customers who are neurodivergent, we have introduced additional ways for customers to contact us and ensure all our communications are fully accessible. We are proud to be part of Neurodiversity Week 2023 with so many companies working to make a difference.”

Kennedys partner and global board member Ingrid Hobbs said that the company celebrates all forms of diversity, whether it’s visible or less visible, and that it values differences and works hard to create an environment where everyone can be themselves and thrive.

“This is why we have partnered with GAIN to help us raise awareness around the topic of neurodiversity and make our workplace more accessible and welcoming to all our people and clients,” Hobbs said.

Just Group chief financial officer and executive sponsor for disability and neurodiversity Andy Parsons said that the company is passionate about creating a diverse and inclusive workplace. He also noted that people from different backgrounds and experiences are integral to Just Group’s success and innovation, and it will help the company serve their customers better now and in the future.

“Neurodiversity is an important strand of our focus on DE&I, and we are proud to be partnering with GAIN to learn more about neurodiversity and how best to support our people in the workplace. We’re delighted to be joining in with Neurodiversity Celebration Week as part of ensuring all our colleagues feel included, valued and able to thrive,” Parsons said.

Phoenix head of workplace distribution and relationships for standard life Emma Furlonger said that the company is passionate about helping people secure a life of possibilities, which it believes is achievable by unlocking the creativity and innovation that neurodivergent individuals can bring.

“We fully embrace neurodiversity and actively champion an inclusive and supportive workplace, for the benefit of customers and colleagues alike,” she said. “We are proud to partner with GAIN and look forward to jointly championing this important topic.”

QBE risk chief operation officer and workability sponsor Rachel Knowles said that by better understanding, supporting, and celebrating neurodiversity, the industry can realize the value of thinking differently.

“We’re delighted to be partnering with GAIN as an Industry Transformer over the next three years, so we can work together to help make QBE and the wider industry a more inclusive place for our neurodivergent colleagues, partners and customers,” Knowles said.

Swiss Re Group head of tax Michael Ludlow said that inclusion, diversity, and equality are fundamental in attracting the best people and making the firm a great place to work.

“As an organisation, supporting GAIN and being involved from the start is exciting for Swiss Re,” Ludlow said. “We are proud to be a part of an alliance of people and businesses who are committed to ensuring neurodiversity is recognised, supported, and celebrated within the industry. Swiss Re is committed to making the world more resilient and we need the best people to achieve this mission.”

UnderwriteMe CEO James Tait said he was proud of the company’s status as one of the founding members of GAIN, noting that the industry-wide initiative will positively impact lives and improve workplaces for the benefit of all.

“We’re passionate about creating a diverse team which is both inclusive and supportive of one another,” he said. “We also see the need to be able to tap into new ways of thinking to solve the challenges that our industry has, to ensure our insurance products and the industry as a whole is truly accessible to all.”

Zurich CEO Tim Bailey said the firm’s people were its most important asset, and that their varied skills, perspectives, and experiences help drive innovation. This in turn makes Zurich more committed to creating an inclusive workplace where all employees can thrive.

“Through our partnership with GAIN, we aim to not only become a more inclusive organisation for our neurodivergent employees, but also to champion neurodiversity at an industry level, helping to make insurance more accessible to our customers and colleagues,” Bailey said.

What are your thoughts on this story? Please feel free to share your comments below.

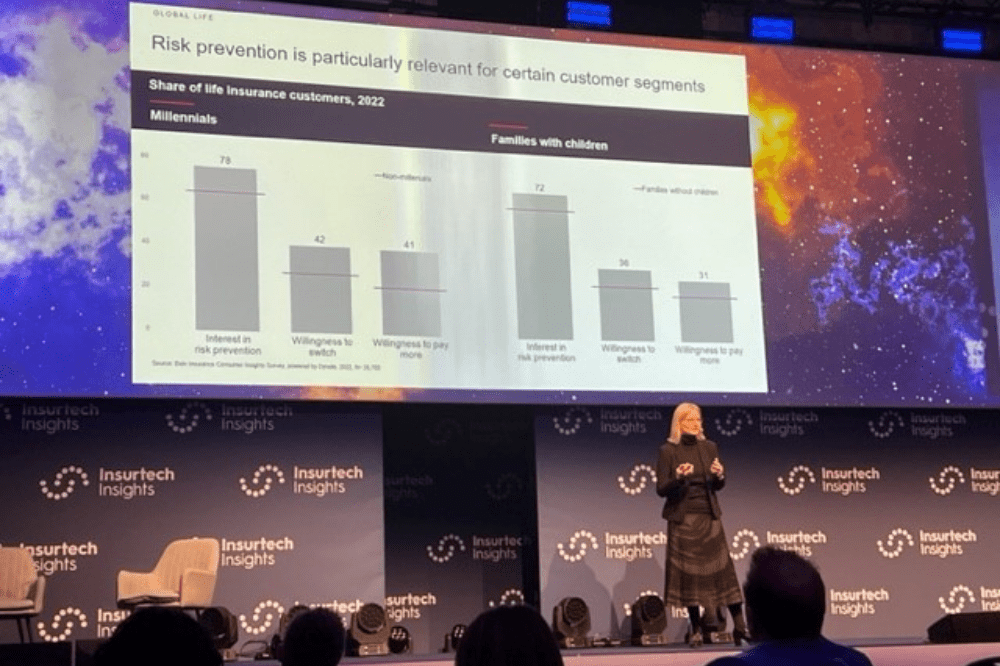

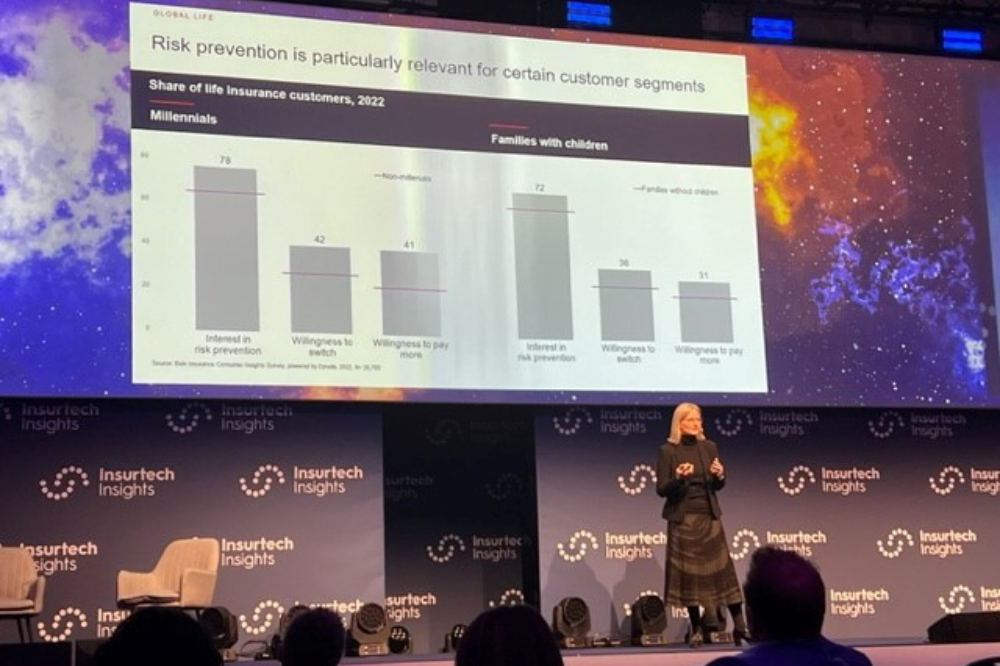

Consumers are looking to insurance companies to act on the world’s biggest challenges, such as climate change, ageing populations, and healthcare gaps. They also strongly want to reduce risks in their lives, according to Bain and Company’s survey.

A majority (80%) of consumers said they want insurers to embed environmental, social, and corporate governance (ESG) initiatives into their proposition. More than half (59%) would like insurers to reward them for healthy living.

Although respondents expressed an overwhelming preference for risk prevention services in auto, home, life, and health insurance, few use the current offerings in the market.

Only 4.3% in the US said they took up the services from their insurers, while figures were dismal for Singapore (4.1%), Switzerland (2.7%), Japan, (2.5%), and the UK (2.1%).

Bain and Company, a global management consulting firm, commissioned the survey from Dynata, which polled 28,765 respondents in 14 countries.

“Consumers need more. The [traditional premise where] insurance just provides capital for covering losses doesn’t satisfy anymore,” said Tanja Brettel (pictured above), practice executive vice president at Bain and Company, at the Insurtech Insights Europe conference in London earlier this month.

Consumer interest in ESG has risen partly due to intense turbulence and uncertainty in recent years, according to Bain and Company’s report.

“Extreme weather events, disease and the Covid-19 pandemic, ageing populations, and technological disruptions are combining to radically change the risk landscape, both through more risks and different types of risk,” the report said.

The confluence of all these factors has triggered an identity crisis for insurance companies as they face heightened demand over what Bain and Company calls the “functional elements” of their value proposition.

Reducing risk, bringing ease and convenience, and paying out claims are just a few of the core offerings that consumers expect their insurers to deliver. But companies must quickly evolve to offer better social impact, life-changing, and emotional value to stay relevant.

“It’s so hard to get the basics right. But consumers still want more,” Brettel told the audience at Insurtech Insights Europe.

“They want to be rewarded, they want companies to be ethical, and they want their insurance company to invest in their wellbeing.”

Why are risk prevention services from insurers not connecting?

Risk mitigation and prevention is the new frontier for insurers, according to Bain and Company’s report. But if consumers want to be proactive about reducing their risks, why aren’t they leveraging services by their insurers?

It might be because many risk prevention offerings are centred on the insurance policy and not the customer, said Brettel.

One case study has demonstrated the power of an insurance service that keeps the focus on customer needs. Life and health insurer AIA’s Vitality app saw more than 300,000 sign-ups in the first year it launched. The app, which caters to young families in Thailand, offers wellness information, trackers for family events and vaccines, and online parenting forums.

“They started with the customer, and not by thinking of ways to get their products in the world. They picked a segment with unmet needs and tailored their offering around it,” Brettel said.

From “push” to “pull” distribution model

As insurers redefine their role and value in the market, agents and brokers have a key role to play.

According to Bain and Company’s report, carriers will need to shift their distribution model from “push” (which focuses on acquisition) to “pull” (which uses data and analytics to address customers’ needs and priorities).

This means brokers and agents will see their ways of working changing dramatically, spending less time on low-value tasks and homing in on building relationships with their carrier partners.

“In many markets, the traditional sales force plays an incredibly important role, not only to drive adoption, but also to create more sales and convert from online to offline,” said Brettel.

Redefining the role of insurance

The shift to risk prevention and purpose-driven business will take time for most organisations. Brettel warned leaders shouldn’t expect immediate profitability from this pivot. But she stressed that the long-term result will be worth it.

“Don’t expect it to be profitable in year one. It takes patience to build that. What’s important is that you focus on defining what your path to monetisation is,” she said.

“This is about the customers. This is about redefining the value you deliver to customers. Customer desirability should be front and centre.”

Do you agree with Bain and Company’s findings on insurance customer expectations? Share your thoughts below.

Botello believes that investing internal resources into diversity, equity and inclusion initiatives can have an extensive effect on business operations at a micro and macro level.

“I think our industry will be committed to this endeavour, not just because of social justice movements, but because it’s the right thing to do and there’s a business case for diversity and inclusion,” Botello said. “I strongly believe more equitable teams create extra value for clients and businesses alike.”

While establishing and sustaining an inclusive work culture that benefits a business and its employees may at times be arduous, she said, “it has proved to be a worthwhile endeavour.

“Here at Marsh, we seek to create that environment,” Botello said. “And obviously, it’s not perfect, and we are not seeking for perfection. We know we will get it wrong sometimes, but what we want is to make people feel that they shouldn’t be scared to get it wrong.”

For Botello, DE&I is “all about learning and being brave.”

“Marsh and McLennan has been around for 150 years, but it is our responsibility to shape progress for the next century,” Botello said.

Creating a balanced workplace

The insurance realm has been a historically male-dominated space that can be intimidating to break into, especially for women. The lack of female professionals in all areas of a company, especially executive-level positions, can deter prospective talent who may not envision upward mobility.

“We must focus on representation at the senior level to make sure that you are effecting change from the top down,” Botello said. “We must also provide training to colleagues so that they can better understand what their biases are to really build equity and inclusion into processes like recruitment and promotion.”

There is also the question of how to make working for an insurance company seem appealing to women and ultimately attract them into the field.

“We are certainly up against stiff competition from other professions that seem more appealing, whether that is teaching or engineering or economics,” Botello said. “You never really hear about a young woman aspiring to be an insurance professional at a young age, and that is something we really need to address to create meaningful change.”

Outreach programs are one option to showcase how a career in this field can be rewarding and stimulating with real opportunities for growth. It is also imperative that in an age of career swapping due to COVID and more favourable remote work positions, a company really needs to impart a sense of value in its employees who could potentially be looking elsewhere.

“I think it is fascinating to explore this topic in-depth to find meaningful solutions,” Botello said.

Reflecting on memorable initiatives

Botello has felt a calling to use her position as a DE&I specialist to create substantial change and opportunities for individuals who may feel neglected by professional industries. While systemic issues abound for various BIPOC and LGBTQIA+ individuals, as well as women, Botello is ultimately proud of her involvement in helping to address and rectify these longstanding injustices in any way she can.

Throughout her time at Marsh & McLennan, Botello is most proud of her involvement in its ‘Leading the Change’ initiative. Created in 2020, the company pledged $5 million over three years to support select organisations that advocate for greater equality for the Black community and double the impact for colleagues who donate to racial justice organisations through a double matching program.

“We also established concrete actions to advance racial justice including establishing a global black colleague network and a race advisory council,” she said.

One of the organisations that they supported was Gideon’s Promise, which is committed to transforming the criminal justice system by building a movement of public defenders who provide equal justice for marginalised communities.

“The funding that we are providing is used to support a program called PIPED, which stands for Public Interest Professionals Expanding Diversity,” Botello said. “It was designed to help build stronger relationships between the legal system and marginalised communities while also giving scholarships to public defenders.”

“This is one of the main challenges of the American criminal justice [system],” she added. “There’s a lot of work and not many well-trained public defenders. So we’re trying to fix that through this partnership.”

The company has also supported the Better Chance initiative, which connects connect middle and high school students to opportunities that help them gain placement in competitive educational institutions.

“The funding that we are providing will directly help over 2000 students a year, establishing vital career platforms while connecting them to employers that are seeking more diverse talent and looking to promote equity in our communities,” Botello said. “I think supporting our communities throughout life’s various challenges is more important than ever, which will then foster responsible business structures to ensure that diversity, equity and inclusion is available for all.”

Intangic MGA said in a press release that the CyFi product is meant to complement and strengthen existing cyber indemnity cover, not replace it. The product also does not have a claims adjustment, and in the case of a material breach, policyholders can expect a fast payout in days as opposed to months.

“A high-frequency risk”

Intangic MGA has analysed thousands of corporations over several years, and in the process found that companies struggling to manage the financial impact of cyberattacks have a 250% higher probability of suffering material losses than peers who had better cyberattack management. This new cyber parametric policy is designed to address the problem of constant cyberattacks as early as possible to lower the probability of customers suffering losses from attacks.

Intangic MGA founder and CEO Ryan Dodd (pictured above) attributes this to a difference in thinking about the problem.

“The security teams at large corporations have to manage cyber threats all day, every day. Our approach assesses cyber as a high-frequency risk. By accepting cyber attacks as ‘constant’, we can measure a link between how these attacks are managed and the financial impact they have on corporate operations,” he said.

According to Dodd, CyFi’s parametric triggers make this link visible, enabling fast recovery from covered material breaches. He also said the product has converted cyber risk to a language that the board of any company can understand.

AXA XL UK and Lloyd’s chief underwriting officer Luis Prato said that CyFi represents a simple solution to a complex problem.

“Intangic’s policy and the mechanisms behind it create a different way to approach risk and unlock capacity for cyber for large public corporations, helping them to strengthen their cyber risk programme,” he said.

In this article, Insurance Business sheds the light on common queries you may have about life insurance in the UK. Questions such as “What is life insurance?” and “What are the types of policies available?” are among those that we will provide answers to. For the mortgage professionals who make up our core audience, this article could serve as a good reference for any clients of yours who have questions about how life insurance in the UK works.

Just like in other countries, life insurance plans in the UK provide a lump-sum payment to the beneficiaries either at the time of the policyholder’s death or after a set period. This financial benefit has made life insurance one of the most popular forms of coverage in the UK.

Your life insurance policy will remain in-force for as long as you meet your premium payments on time. Depending on the type of plan you choose, your coverage can end after a set term or last a lifetime.

You can likewise pick between two types of cover:

1. Single life insurance policy

This type of life insurance plan covers only one person and pays out the death benefit if they die during the length of the policy, at which point coverage ends. Some couples opt to take out separate policies, so they will still have coverage even after their spouse or partner dies.

Single life insurance benefits are also paid into your estate, allowing you to choose your beneficiaries. We will discuss life insurance beneficiaries in detail later.

2. Joint life insurance policy

A joint policy covers two lives, but only pays out after one person dies, after which coverage ends. The death benefit goes to the surviving partner, unless other arrangements were made.

If a couple with a joint life insurance plan separates, they may be able to convert this into two single life insurance policies.

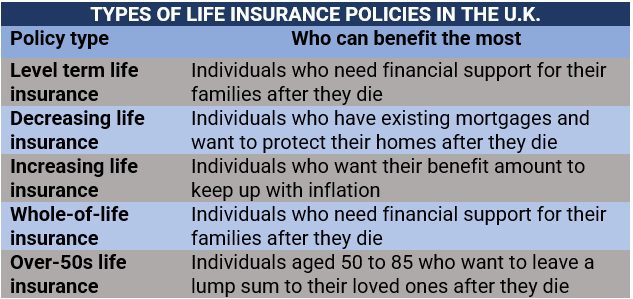

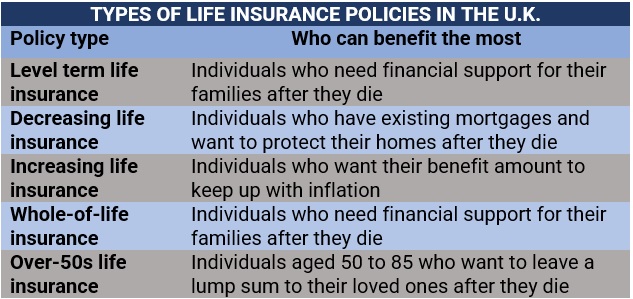

Insurers offer different types of policies, with each offering varying levels of financial protection. In general, life insurance plans in the UK come in two major categories. These are:

1. Term life insurance

As the name suggests, term life insurance policies run for a fixed term. You are free to choose the coverage amount and policy length but bear in mind that your choices have a corresponding impact on premiums. Term life insurance pays out a benefit only if you die within the set timeframe. Otherwise, the insurer keeps all the premiums you paid. Some providers, however, also cover you if you become terminally ill.

If you’re considering taking out term life insurance, there are three types of plans you can choose from. These are:

Level term life insurance: Or simply life insurance, pays out a lump sum if you pass away within the agreed term, with the level of cover remaining the same throughout.

Decreasing term life insurance: This type of policy is often used to pay off your mortgage, that’s why it is sometimes called mortgage protection insurance. The death benefit amount reduces each year to correspond with your loan balance, although your premiums remain the same.

Increasing term life insurance: The death benefit amount in this type of policy increases throughout the plan’s term to keep up with inflation.

2. Whole-of-life insurance

Whole-of-life insurance, also called a life assurance plan, provides lifetime coverage, with the payouts given to your beneficiaries after you pass away. Because of the level of coverage this policy provides, the premiums are also more expensive compared to those of term life plans. One major drawback is that if you live longer than expected, you may end up paying more than what you can get out of the policy.

And just like whole life insurance in the US and Canada, this type of life insurance in the UK sometimes includes an investment element that you can access while you’re still alive and can be sold through financial advisers.

Term life insurance. Whole-of-life insurance. These are just some of the buzzwords you’ll encounter when taking out life insurance in the UK. If you want to know the meaning behind the different life insurance jargon, our glossary of common insurance terms can help.

Over-50s life plan

Not considered a major category, some UK life insurers offer over-50s life plans, which provide coverage for individuals between 50 and 85-years old. Premiums are based on the benefit amount and the policyholder’s age. These plans also offer guaranteed acceptance, meaning applicants are not required to submit medical information. Because of this, rates are often higher as insurers have no way to predict the plan holder’s risk level.

Over-50 plans’ are typically capped at around £20,000. There is also a waiting period that can range from 12 to 24 months. If the policyholder dies due to natural causes within this period, the beneficiaries will not receive a benefit but the premiums they paid will be returned.

Who needs life insurance?

While not everyone may need this form of coverage, there are certain types of individuals and groups who can benefit the most from taking out life insurance. They include:

Breadwinners

Parents of school-aged children

Parents who have dependants with special needs

Families with existing mortgages

On the other end of the spectrum are individuals who do not need life insurance, including:

Singles

Those whose spouse or partner earns enough for their family to maintain their lifestyle

Low-income earners who can qualify for state benefits

Some employers also offer employee packages that include death-in-service benefits – which work somewhat similar to life insurance – with a coverage amount linked to your salary. That’s why it pays to check with your company to see if you already have cover. However, you may still need to take out a life insurance policy if you feel that the benefits you are eligible for are not enough to sustain your family’s lifestyle after you die.

Another thing to remember is that employee packages are non-transferrable. This means that when you leave your employer, you cannot take the benefits with you.

The table below sums up the different types of life insurance in the UK and who can benefit the most from each.

A pre-existing condition does not necessarily prevent you from taking out life insurance in the UK but there are some additional factors you need to consider. These include:

The insurance company may require additional medical information: Insurers may require you to undergo further screening and medical examinations to learn more about your condition. Some providers cover the cost of these tests.

Your premiums may cost more: If you get approved, your insurer may charge higher premiums, depending on the severity of your condition, as you also present a higher risk.

Another option is an over-50s plan, which offers guaranteed acceptance. These plans, however, do not provide the same level of coverage as standard life insurance policies and can even cost higher.

During the application process, your insurer will ask you several lifestyle- and health-related questions to determine your risk level. It is very important for you to answer these questions accurately and honestly, and to disclose any pre-existing medical condition.

Your insurance provider regularly checks the medical information you provided and may contact your doctor for confirmation. If you have been found to deliberately withhold important medical details from your insurer, they may cancel your policy and void coverage.

As the policyholder, you can name anyone as a beneficiary of your life insurance plan. These include:

You can also name the beneficiaries as an individual or group. If you have a single life insurance plan, the benefits will be paid into your estate, where the beneficiaries are named through your will. If you do not leave a will, the proceeds of the estate will be shared according to the rules of intestacy.

You can likewise name beneficiaries when you place your life insurance in a trust. Doing so has potential benefits, including:

The benefits will not be counted as part of your taxable estate, meaning the lump sum will be passed on to your beneficiaries exempt from Inheritance Tax (IHT).

The benefits can reach the beneficiaries faster if there are appointed trustees who will take care of the process after you die.

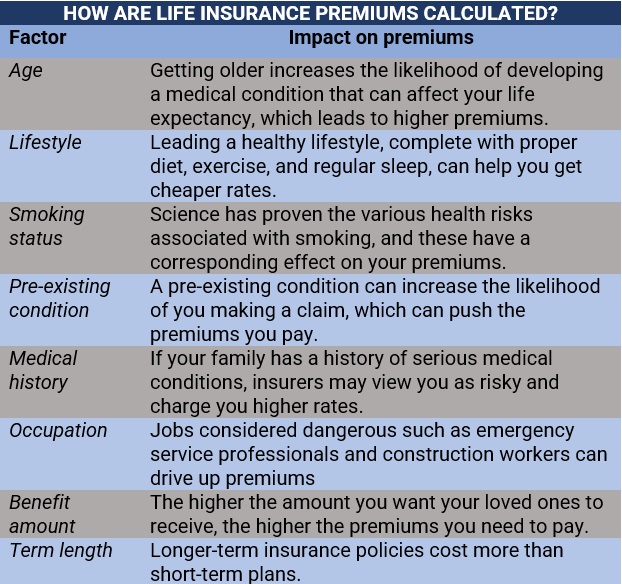

Because each person’s lifestyle and health status vary significantly, it’s difficult to provide a ballpark figure to represent the cost of standard life insurance in the UK. Premiums are influenced by a range of factors. The table below sums up these parameters and how they impact life insurance rates.

The answer to this question depends on your personal situation. If you have people who are heavily reliant on you financially, then life insurance can help provide some level of monetary support after you die. Taking out life insurance can also help pay off your mortgage if your beneficiaries do not have the financial capacity to do so.

Not everyone, though, needs this type of coverage. If your wealth is enough to maintain your loved ones’ lifestyle after you pass away, then purchasing life insurance is unnecessary. It’s the same if you are single with no dependents.

If you want to know how life insurance policies work in different countries, you can check out our global life insurance primer.

An experienced insurance agent or broker can give you a rundown of the types of coverage that best fits your personal circumstances. We recommend that you check out our Best Insurance for UK page to find reliable and trustworthy insurance professionals near you.

The insurance companies featured on this page are nominated by their peers and vetted by our team of experts as reliable leaders in the industry. By dealing with these providers, you’ll have the peace of mind of knowing you’re getting the best coverage from someone who can be trusted during difficult times.

Are you searching for the right life insurance plan? Which features and benefits do you think are important? Share your thoughts in the comments section below.

UK chartered insurance broker Verlingue has announced the hiring of Jon Bethell as its head of private clients. The appointment is part of the broker’s plans to rapidly expand and grow its existing high-net-worth (HNW) offering.

In this new role, Bethell will use his specialist expertise to develop a market-leading HNW proposition at Verlingue, as well as delivering new growth and development opportunities.

“A real asset to Verlingue”

“Jon is a real asset to Verlingue as we look to build out our existing private clients business. He has over a decade of experience in this sector and already has very strong relationships with many of our key insurer partners. His experience of building high performing insurance teams based across multiple locations will also ensure we can deliver on our ambitious growth targets in this sector,” Verlingue CEO Mike Latham said.

Bethall has two decade’s worth of insurance experience. His most recent posting before the UK broker was with insurer Hiscox, where he worked for 12 years in supporting some of the country’s largest brokers. He last managed the trading team at Hiscox. Before that, his roles included claims and underwriting functions at Ageas and Aviva, respectively.

The firm also recently created a dedicated media practice, headed by client director Maia Olesen – a move corresponding with plans to expand Verlingue’s presence in the fast-growing independent media sector.

What are your thoughts on this story? Please feel free to share your comments below.

Through this new capacity, Coalition is set to help more businesses get the coverage that they need in order to better protect themselves from digital risk. The insurer will extend its reach to provide full-follow form coverage and protection of up to £10 million above a primary layer of insurance from another insurer for both cyber and technology professional indemnity (PI) lines.

Greater reassurance with state-of-the-art prevention technology

“Our new excess product is designed to help UK brokers struggling to find enough cyber and tech PI protection for their clients. By bringing in Coalition to provide excess cover, brokers give their clients greater reassurance with our state-of-the-art prevention technology and early threat warnings from our 24/7 internet scanning operation,” said Tom Draper, UK head of insurance for Coalition.

The excess policy from Coalition provides the added benefits for policyholders of access to Coalition Control, the insurer’s proprietary attack surface monitoring technology that delivers personalized risk assessments, in addition to advice from Coalition’s in-house incident response cyber support team. Allianz and Lloyd’s of London will support Coalition’s policies.

Coalition also offers excess of loss cyber products in the US and Canada. Interested brokers can submit directly to Coalition’s underwriting team and find out more through the official site.

Insurance telematics solutions provider Trakm8 has commissioned a new national driver survey that revealed some insights on the cost of living, technology, and other factors that impact how drivers purchase insurance.

The survey found that 69% of UK drivers expect to drive more miles in 2023 than last year. Seven out of 10 (70%) of them also expect their mileage to be higher than pre-pandemic levels. Additionally, more than half (58%) of the survey’s respondents said that they are considering a telematics insurance policy to reduce costs associated with car usage and mileage increase.

Survey results are “fairly surprising”

The survey yielded some “fairly surprising” results, Trakm8 insurance managing director Adam Gooch said, as it did not align with the expectation that the rising cost of living would “impact the number of insured vehicles on the road and total mileage expected to rise in 2023.” Additional information from the survey showed that very few households in the UK – equivalent to 9% – will be reducing the number of insured cars due to the cost of living.

Trakm8 collaborates with some of the country’s leading insurers as a provider of telematics policies. The firm’s end-to-end solution includes a portal that provides instant driver and vehicle insights such as journey information, driver scoring/alerts and vehicle health, as well as an app that gives drivers an easy-to-use interface with an overview of their driver data and scoring.

“It is really positive to see so many more drivers receptive to a telematics policy to reduce costs and reward good driving. Our comprehensive end-to-end insurance telematics solutions are designed to give insurers a unique opportunity to help personalise policies based on a customer’s habits and requirements,” Gooch said.

What are your thoughts on this story? Please feel free to share your comments below.

The schemes market is full of highly lucrative opportunities and brokers all over the world want to get in on the action.

Join Simon Medhurst for a deep dive into the schemes market and the value of brokers getting involved. Learn how to provide exceptional value tailored to your clients’ needs, the advantage of a partnership-first approach and a robust framework, and how Travelers 4D (discovery, design, delivery & development) process works to create a great scheme.

By the end, you’ll understand the secret recipe for a successful scheme and how brokers can harness these exclusive opportunities.

Understanding the schemes market has never been easier. Don’t miss this informative podcast and everything it has to offer on the schemes market.

We use cookies to ensure that we give you the best experience on our website. If you continue we will assume that you are happy with it.AcceptPrivacy Policy