The partnership further builds on a successful collaboration that has delivered improvements within the industry, including customer retention, safe driving, and fraud detection. The lab aims to develop real-world solutions to tackle various significant challenges in society, from sustainability to autonomous mobility.

“Developing cutting-edge insurance and services”

“Insurance was born in the UK and breakthroughs of many kinds have their origin here, so it’s the perfect place for our new hub of innovation,” ANDI president Keisuke Niiro said. “The Aioi R&D Lab aims to solve global-scale social issues through developing cutting-edge insurance and services utilising AI technologies.”

Niiro said that the lab will combine the capabilities of Oxford researchers, the AI provided by Mind Foundry, and the insurance capabilities of Aioi Nissay Dowa Insurance to develop solutions for significant societal challenges.

“Coming together as ‘One Team,’ I am confident Aioi Nissay Dowa and the experts in the Oxford ecosystem can offer solutions that will have a tremendous impact on the world,” Niiro said.

“We have made a long-term commitment to invest in cutting-edge innovation in the development of new insurance models, products, and services – not just for our own benefit, but to create a shared value that solves social and community issues across all parts of society,” AND-E group CEO Michael Kainzbauer said. “Insurance is pivotal to mitigating and protecting people from the impact of some of the biggest issues facing our planet and our populations, and we are excited to be working with Mind Foundry to take some big strides towards practical solutions that will drive change at a massive scale.”

The lab will focus on several topics that create shared value across society, including:

Developing products that insure individuals continuously across multiple modes of mobility, including cars, trains, scooters, etc. This is to reduce risk, traffic accidents, and CO2 emissions

Developing models of insurance for autonomous vehicles, a field where insurers need to understand a vehicle’s sensors and the complexities of how self-driving algorithms are configured

Developing the next generation of telematics-based insurance, as well as personalised insurance and insurance for artificial intelligence

Developing solutions to reduce carbon and energy use in transport, preserve biodiversity, and gain a better understanding of the risks associated with climate change

Developing solutions to help deal with aging populations, as well as extend wellness and health care

“Big knowledge,” not just “big data”

On the board of the newly formed lab are key representatives from AND-E and Mind Foundry. Kainzbauer will chair the board while AND-E executive manager Jun Ikegami will take the post of CEO. The two will work alongside Mind Foundry CEO Brian Mullins and ANDI representatives from the ANDI holding company, Masauki Yazawa and Kuniaki Uehara.

Supporting the board is an advisory panel of professors from the University of Oxford, each with different expertise across many disciplines that sit at the heart of the transformations facing society, with particular focus on insurance. These include Mind Foundry co-founders professor Stephen Roberts and professor Michael Osborne. The rest are as follows:

Michael Wooldridge, professor of computer science at Oxford University

Malcolm McCulloch, associate professor in engineering science and group leader of the Energy and Power Group at the University of Oxford

Paul Newman, who leads the Oxford Robotics Institute

Baroness Kathy Willis, professor and principal at St Edmund Hall and professor of biodiversity in the Department of Zoology, University of Oxford

Doyne Farmer, Baillie Gifford professor of mathematics

The lab’s aim is to build a better understanding of the data that surrounds us and identify ways in which truly informative “big knowledge” can be extracted from that information, and not just the “big data,” according to Stephen Roberts, Mind Foundry co-founder and professor of machine learning at University of Oxford.

“Big data is useful up to a point, but what we need now are very smart algorithms that can distil that data into knowledge that is interpretable, valuable, understandable, and beneficial to everybody,” Roberts said. “We want to understand the societal impact – not just of insurance, but of risk, environment, and sustainability – and form a foundation for how algorithms of all levels of sophistication can work in harmony with society.”

“Mind Foundry is dedicated to tackling high-stakes problems with AI – and the insurance sector is not only one that impacts all of our lives both individually and at scale, but it’s also at the forefront of long-term thinking about global economic problems and the effects of change on people and civilization,” Mind Foundry CEO Brian Mullins said. “We could not have better partners as we take on some major challenges in that field with this R&D lab.

“Aioi Nissay Dowa shares our aspirations and understands the importance of digital transformation working with – not against – society, and we will also benefit from the University of Oxford’s rich ecosystem, which has been at the cutting edge of AI research for decades,” Mullins said. “We look forward to deepening our relationship with ANDI and the University of Oxford and working together to create a more inclusive and fairer world for all.”

Besides the advancement of AI, several new breakthroughs have also been introduced within the insurance business. Recently, specialist insurer CFC announced the implementation of policy encryption within its products, providing an additional layer of security for its customers.

What are your thoughts on this story? Please feel free to share your comments below.

“Our future success at MS Reinsurance will be defined by our ability to expand our customer-centric approach and provide our valued partners with bespoke, innovative, and efficient solutions,” MS Reinsurance CEO Robert Wiest said. “I am delighted to welcome Benedikt, Susanne, Marcus, and Stefan to MS Reinsurance. All four join our growing team as we embark on our next chapter. We are committed to investing in our people and with more than 75 years of specialist experience, collectively, we are excited about the expertise they bring to the MS Reinsurance team.”

Gnädinger took her post on November 1, reporting directly to Wiest. Her current role sees her spearheading the recently rebranded business’s modernization journey. She has a previous 17 years of experience with Partner Re, developing deep expertise in business processes, systems design, and integrating new technologies for reinsurance.

Schmid was appointed on February 1, also reporting directly to Wiest. With 24 years of experience in the reinsurance industry, he was previously the chief information officer at AXIS Re. His new role within MS Reinsurance will see him leading the implementation of the reinsurer’s IT strategy aimed at improving the use of data and technology to support the business.

Pollak also joined the reinsurer on February 1, and he now reports to chief technical underwriting officer Grégoire Mauchamp. The newly created role sees Pollak leading the underwriting operations team and supporting a wide range of products and processes globally across various geographies. Pollak previously lead the global underwriting support team at AXIS Re.

Finally, Behr will officially start his tenure at MS Reinsurance on March 1, reporting to EMEA chief underwriting officer Jörg Bruniecki. Behr will bring with him a blend of business development, client management, and underwriting experience. He recently held the head of business development post EMEA at Swiss Re.

The surge of appointments comes months following MS Reinsurance’s rebranding from MS Amlin AG, a move in-line with parent company MD&AD’s commitment to forming a globally diversified reinsurer.

What are your thoughts on this story? Please feel free to share your comments below.

European property and casualty (P&C) insurance run-off group Marco Capital Holdings has announced its acquisition of Navigators International Insurance Company (NIIC) from its previous parent company, The Hartford Financial Services Group. The transaction is still pending and subject to regulatory approval.

A UK-based insurance company, NIIC is authorised by the Prudential Regulation Authority and the Financial Conduct Authority. It was established by The Navigators Group, which was acquired by The Hartford in 2019.

Completing The Hartford’s exit from Continental Europe

NIIC has a small amount of legacy business based in run-off, which comprises property and casualty, marine, and professional liability insurance business. These are predominantly based in Continental Europe, within the countries of Belgium, France, Italy, the Netherlands, and Spain as well as the UK.

Marco Capital’s purchase completes The Hartford’s exit from Continental Europe. That said, The Hartford will continue to serve the international market through its NIC UK Branch and Hartford Syndicate 1221 at Lloyd’s.

“We are delighted Marco has been able to assist The Hartford in achieving its strategic objectives with regards NIIC,” Marco Capital CEO Simon Minshall said.

In May of last year, Marco Capital completed its acquisition of the insurance businesses under Capita, in particular its specialty insurance businesses Capita Commercial Insurance Services Limited (CCIS) and Capita Managing Agency Limited (CMA). Marco has rebranded the acquisition under the new name Polo, which is also a play on the Marco Capital Holdings name. The newly christened group is backed by €500 million equity committed by Oaktree Capital.

Digging into the key financials shared by Allianz Holdings, Holmes revealed that GWP is up about 4.4% across the business to about £3,966 million. Allianz Personal has reported a 3.6% rise in GWP to £2,635.4 million while Allianz Commercial is up 6.4% to £1,330.2 million.

However, reflecting the challenging trading conditions registered by the market in 2022, the operating profit of the business dropped 58.3% to £132.3 million, down from £317.6 million in 2021 while its combined operating ratio rose 6pp to 99.2%.

Behind the operating profit decrease

Examining the causes of this operating profit decrease, Holmes pinpointed that the UK market saw some of its worst weather conditions in 2022 with three storms in February alone and subsidence losses as a result of the summer heatwave – capped off with a December freeze that resulted in high escape-of-water losses in household and also saw increased frequency and severity in motor claims due to the impact of the freeze on drivers.

“But in 2022, by far the greatest impact on our results was the impact of inflation,” Holmes said in a media briefing with Insurance Business UK. “This was driven by supply chain issues, the energy crisis, and labour shortages. These have all had a knock-on impact on our business, both our prior reserves and our current-year loss ratios.”

He noted that the significant growth and improvement seen across a number of lines of business with Allianz Holdings was offset by the impact of inflation. Overall, Allianz experienced gross inflation of 9.5%, which was ahead of predictions and pricing assumptions made at the beginning of 2022. But looking at collision and accidental damage, he said, the inflation rate actually registered as being in the 20s in terms of its impact due to supply chain concerns.

“Inflation is something that we saw very early on in 2022,” Holmes said. “But our expectations and that of the Bank of England was that it would peak earlier and then come down very quickly. I think we all now accept that inflation went higher than anybody’s expectations and it’s likely to stay with us far longer than was originally anticipated.

“There’s a number of things we do to mitigate that. We obviously have supply chain contracts with a lot of our providers that have fixed pricing within them. We look at our entire cost base to see where we can eliminate costs. We have been working with a number of companies to look at Green Parts as replacement parts for vehicles, to reduce the cost of the impact of vehicle damage etc. And we’ve looked at how to fill labour shortages by using the extensive reach of the Allianz group.”

As part of a large global insurer, the business is lucky to be able to access enhanced resources that help it alleviate many of the supply chain pressures facing the wider market but Holmes highlighted that it is not possible to mitigate inflation to the extent of completely eliminating its impact on claims. As a result, the insurer has also been rating to deal with inflation and to offset its ongoing impact in 2023.

He added that Allianz Holdings expects, “rate to continue to be an issue in 2023 as we deal with the impacts of inflation through increased insurance premiums.”

What 2023 will bring for the business

Despite the challenging market conditions, Holmes highlighted that there is a lot to look forward to as the business faces into 2023 and beyond. He has always maintained that the business’s greatest asset is its people, he said, and Allianz Holdings is “incredibly proud” of the support it has been able to deliver for colleagues to help them navigate the tumultuous external environment.

The business has also continued to develop its relationships with its broker partners and customers alike, with benchmarking research carried out in 2022 confirming that Allianz is No.1 in the market for Commercial Mid-Market, Petplan, LV= and Engineering Inspections. As somebody passionate about strong relationships with brokers, he said, receiving that affirmation that Allianz is maintaining its reputation in both commercial and personal lines for the service it provides has been fantastic.

“Looking forward to 2023, we expect it will continue to be a difficult year,” he said. “Inflation and supply chain disruption will continue to impact on our business – and of course, that will impact on rate in 2023 which we expect will continue to drive a hard market.

“We’ve also been calling on our broker partners to work with us to deal with the issue of underinsurance which we see as a problem that already existed prior to this economic downturn and is worsening as as inflation rises. So, we’re going to continue to work hard with our broker partners in 2023 to deal with the thorny issue of underinsurance in the UK market.”

What are your thoughts on this story? Please feel free to share your comments below.

Among the market updates delivered, the insurance services firm Davies revealed that it has been certified as an agency with the Department of Education to offer “Flexi-Job Apprenticeships.” Bravo Networks also had good news to share, announcing that it has partnered with learning and development company Raise the Bar to offer fully funded apprenticeships to members in England.

Meanwhile, Zurich UK announced that it is offering 100 new apprenticeship places in 2023, in line with its ambition to, “attract young talent and futureproof its workforce.” As part of the initiative, the insurance giant is expanding its current apprenticeship programme to include new placements in HR, marketing and data protection. Though each firm is taking a different approach, at the core of these programmes is the shared ambition to diversify access routes into insurance and to champion people development on an ongoing basis.

While recently catching up with the brilliant Karen Sharpe of the insurance law firm HF, I was reminded of the sheer breadth of insurance-related roles that exist across the market, beyond underwriting, broking and loss adjusting. HF’s line-up runs the gamut from paralegal apprenticeships, to level 7 solicitor apprenticeships, to graduate entry solicitor apprenticeships – while the firm remains one of the only practices operating in the insurance sector to exclusively offer training contracts to existing employees.

Insurance apprenticeships and social mobility

As Karen highlighted during our conversation, critical to conversations around apprenticeships is understanding the capacity that the right training and development opportunities have to move the dial on advancing social mobility. Creating greater social mobility goes right to the heart of HF’s culture, she said, which can be witnessed by the number of senior leaders across the business who have traversed non-traditional routes to the top.

Social mobility in insurance is an element of the diversity, equity and inclusion (DE&I) trifecta that can occasionally dip under the radar, overshadowed by more obvious or urgent considerations. For while age, race, religion and sexual orientation were named protected characteristics under the Equality Act 2010, socio-economic status is not covered.

In an interview with Insurance Business, Zurich UK’s Caroline Dunn discussed the importance of advocating for increased social mobility in insurance, touching on her own experiences growing up in an economically disadvantaged environment.

“I grew up in Wakefield which is quite a poor area and quite different culturally to living and working in London,” she said. “As I was growing up and thinking about what I wanted to do, things like insurance, and careers in the City or in financial services, were difficult to find out about. Certainly, I knew nothing about them.”

As the daughter of a plumber and a secretary, she had no family connection to financial services and has seen first-hand that not having the contacts needed to know what careers and opportunities exist in the market creates an additional barrier to entry for young people. With Caroline’s experiences in mind, the need to carry on conversations around opening up access to insurance and financial services careers to a broader talent pool seems especially critical.

Hearing from insurance apprentices

Of course, perhaps the clearest and strongest voices emphasising the link between apprenticeships and an expanded network of insurance talent are those from the individuals who have themselves seized such opportunities. Ellie Jones, now a senior account handler at Hazelton Mountford, is one such ambassador for the cause.

“It’s an achievable way of getting into a career without having to go to university/college,” she said, “starting from the bottom and working your way up and consistently earning a wage while you learn and grow. By the time my friends were leaving university, I had a career and was earning a good wage.”

The best thing about the development of apprenticeship programmes is they amount to something of a self-fulfilling prophecy. Those who undertake them tend to become their most ardent defenders and, as they progress in their careers, also the finest advertisements possible for the difference these initiatives can make.

What are your thoughts on insurance apprenticeships? Please feel free to share your comments below.

Gross written premium (GWP) in the period amounted to US$20 billion, which is higher than the US$18.5 billion GWP posted for FY21. All three QBE divisions – North America, international, and Australia Pacific – contributed increases in GWP.

“In a backdrop underscored by heightened inflation, geopolitical tensions, and elevated catastrophe activity, QBE’s underwriting performance demonstrated improved resilience, with the adjusted combined operating ratio of 93.7% improving by 1.3% compared to the prior period,” noted QBE in its announcement.

“Strong premium growth continued, with group-wide renewal rate increases of 7.9% in FY22, which supported gross written premium growth of 13%.”

Enstar deal

In its earnings report, QBE also announced a reinsurance deal with Enstar. De-risking QBE’s exposure to reserves worth US$1.9 billion, the transaction is designed to support improved capital efficiency and reduced reserve volatility risk while providing “greater bandwidth” to focus on customer outcomes and sustainable growth.

Separately, in an emailed release, Enstar said: “Enstar’s subsidiaries will assume net loss reserves from QBE of US$1.9 billion and will provide approximately US$900 million of cover in excess of the ceded reserves on business largely underwritten between 2010 and 2018.

“The transaction will complete upon receipt of regulatory approvals and satisfaction of various other closing conditions. Upon completion, a portion of the portfolio currently underwritten via QBE’s Lloyd’s syndicates 386 and 2999 will be transferred into Enstar syndicate 2008.”

QBE highlighted that capital released from the loss portfolio transfer will be reallocated to ultimately support an improved outlook for returns.

It’s never been harder to excel as an employer in the insurance sector.

“This is the most challenging market I have worked in going on 17 years,” says Kieran Boyle, the managing director of CKB Recruitment. “Employers are having to up their game, which is resulting in the employee holding all the cards.”

This is echoed by Nishma Gosrani OBE, partner in the financial services practice at Bain & Co. in London, who explains how important it is to deliver in the current climate. “If you’re spouting something different in your recruitment material to what you actually are, it becomes very obvious.”

“This is the most challenging market I have worked in going on 17 years. Employers are having to up their game, which is resulting in the employee holding all the cards” Kieran Boyle, CKB Recruitment

For Boyle, there are two types of employers. First, companies who have learned from the pandemic to accept flexible working arrangements and to reinvest in their staff. Second, businesses who have resisted change.

“Firms who have not evolved post pandemic are the biggest losers in the talent attraction war,” explains Boyle. “There are stubborn CEOs who for some reason think selling insurance cannot be done – at least sometimes – remotely.”

Positioned squarely in the first category are 2023’s IBUK Top Insurance Employers, 14 award winners whose own employees ranked them highly in areas such as benefits, compensation, culture, employee development, and diversity and inclusion.

Issues in the insurance labour market

For Jo Morgan, associate director of HR at Top Insurance Employer TH March, the main factors influencing the insurance labour market are work-life balance and ensuring proper renumeration.

TH March has had a hybrid policy for a few years and continually monitors it via Pulse surveys.

“We are finding that hybrid working is a top priority for candidates and is often asked even before salary discussions during the recruitment process,” says Morgan.

For the 125 employees across their six branches in the UK, TH March has more than 60 varied working arrangements and 25% of staff who work part-time. Regarding employee wellbeing, 11% of TH March’s employees are trained as Mental Health First Aiders.

This exemplifies the analysis provided by Gosrani, who picks out the most important factor for employers. “The culture of the organization and the culture of senior management, because there is so much more access from graduates on how they can understand their culture,” Gosrani adds how recruitment websites and people keeping in touch with former colleagues means there is an abundance of information for employees to access.

Jenny Cooper, the head of HR at award-winner Flood Re, also asserts that her firm has adapted its ways of working in this environment. “We need to balance business needs with employee expectations and find a way to get this right within hybrid working,” she says.

Meanwhile, there’s the money issue. “One of the main issues I see influencing the employment market within the insurance industry in 2023 are the drastic cost of living increases,” says Morgan. “Salaries need to remain competitive to ensure that we attract, recruit and retain the best employees.”

Cooper adds that it’s important to find and keep the right people in this highly competitive and fast-paced recruitment market. Marcella McLean, the chief human resources officer at Top Insurance Employer Arch International, agrees.

Then there’s diversity, equity, and inclusion (DE&I), which both Cooper and McLean say remains important. “Keeping sight of and a focus on DEI and finding ways to be truly inclusive as inclusion means something different to everyone,” says Cooper.

Again this is something Gosrani stresses is a major factor and says when she speaks to CEOs it “almost always comes up.”

And she adds an example of how important it is across the industry. “We actually worked very closely with a number of insurance organisations, including the chief executive of Aviva, very recently on the Women in Finance Charter blueprint, which has been rolled a large number of Financial Services Organisation.”

What matters to employees

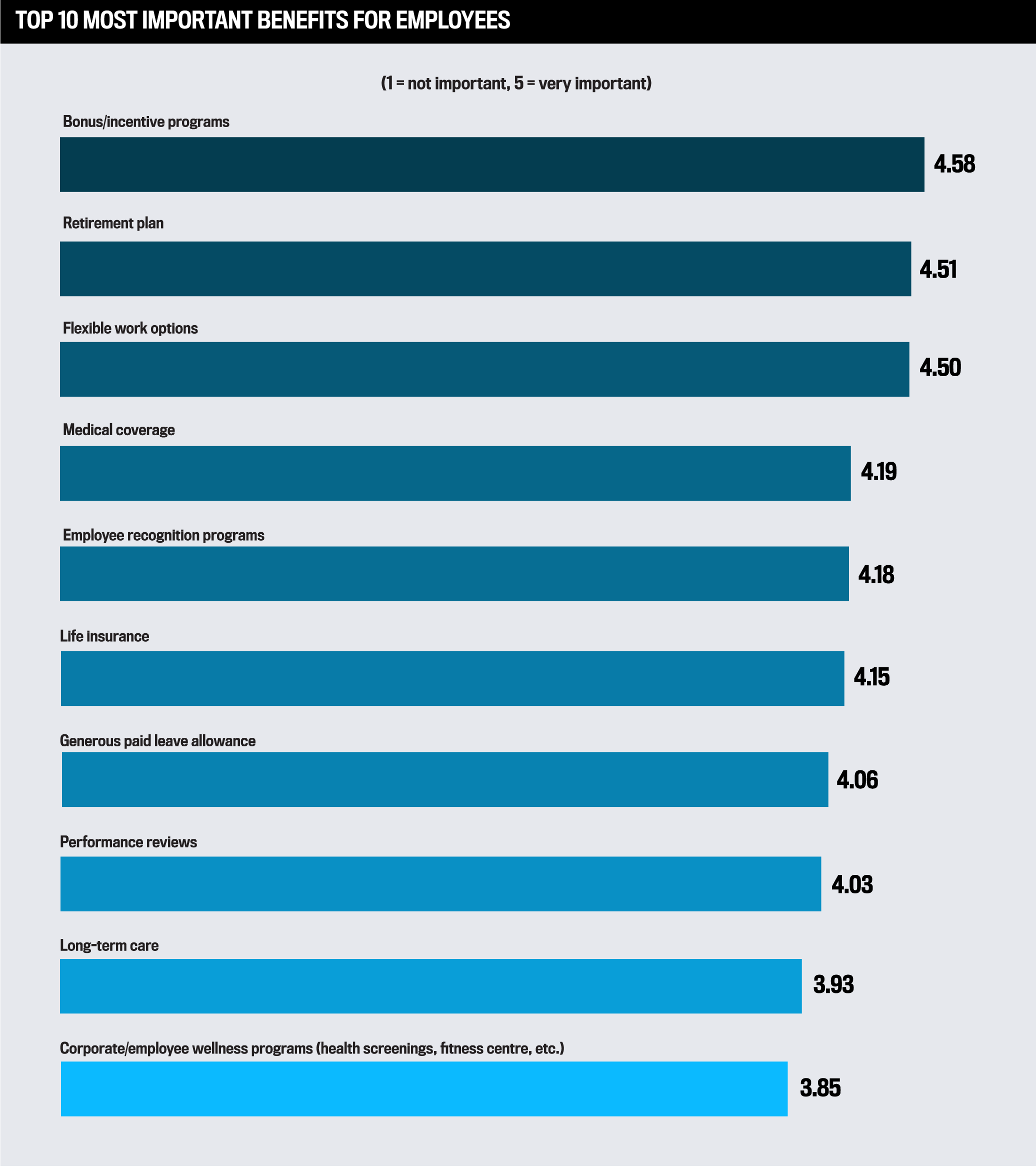

For the IBUK Top Insurance Employers survey, employees ranked the top 10 most important benefits, shown in the box below.

“We are finding that hybrid working is a top priority for candidates and is often asked even before salary discussions during the recruitment process” Jo Morgan, TH March

Regarding the top priority for employees being bonus/incentive programs, McLean explains there has been a shift back to basics. “Whereas in recent years, there had been a greater focus on providing a more holistic range of employee benefits, the current financial climate is undoubtedly seeing a shift in perceived importance to the more financially oriented aspects of the benefit programme,” she says.

In the survey, one of her colleagues at Arch says, “We can always say ‘pay more’ especially in the current economic environment.”

Cooper says retirement plans are something that everyone eventually prioritises. “We ensure our employees have access to comprehensive financial advice and support to maximise all of the benefits available to them,” she says. “We want to make retirement planning as easy as possible and positively encourage people to plan and save for their futures.”

Flexible work options have become integral as a result of the pandemic. However, McLean warns, “It is imperative that we ensure that the integration of flexible working does not hinder the development of the individual employee. In the case of the insurance industry, face-to-face interaction with colleagues and market peers as well as on-site mentoring and training are core parts of the development process.”

As part of the survey, an anonymous Arch employee states, “The work environment is really healthy, and management is friendly, open minded and always available.”

For Cooper, medical coverage through their current private medical insurance provider is paramount. “It’s reassuring to know employees can get quick and easy access to the support and treatment needed when needed without having to jump through unnecessary hoops,” she says.

Lastly, there are employee recognition programs. “It is vital that the hard work and dedication of employees across every level of an organisation are recognised,” says McLean. “Such recognition and reward provide an excellent mechanism for not just motivating employees but also reinforcing a positive company culture.”

Another anonymous Arch employee states that the company values its employees. “I feel as if I’m taken seriously and highly valued within Arch, and this is the first company I have worked for where I’d be happy to stay until I retire.”

“We need to continue to nurture and take care of our culture – in my opinion, culture needs constant attention, it’s not about periodic culture exercises” Jenny Cooper, Flood Re

What could be done better?

Progress is a constant process and not a destination.

Gosrani explains how standout firms gather data from their employees and act on it, which is something being practiced by IBUK’s Top Employers. She says, “So, they are listening on a frequent basis. If you look at some of the CEO changes across the insurance industry, we’re seeing a fundamental shift in type of personality and we’re seeing a lot more women in those senior roles than we’ve ever seen before, but also the old group of male CEOs that used to almost run that part of the industry have now moved on NED roles etc.”

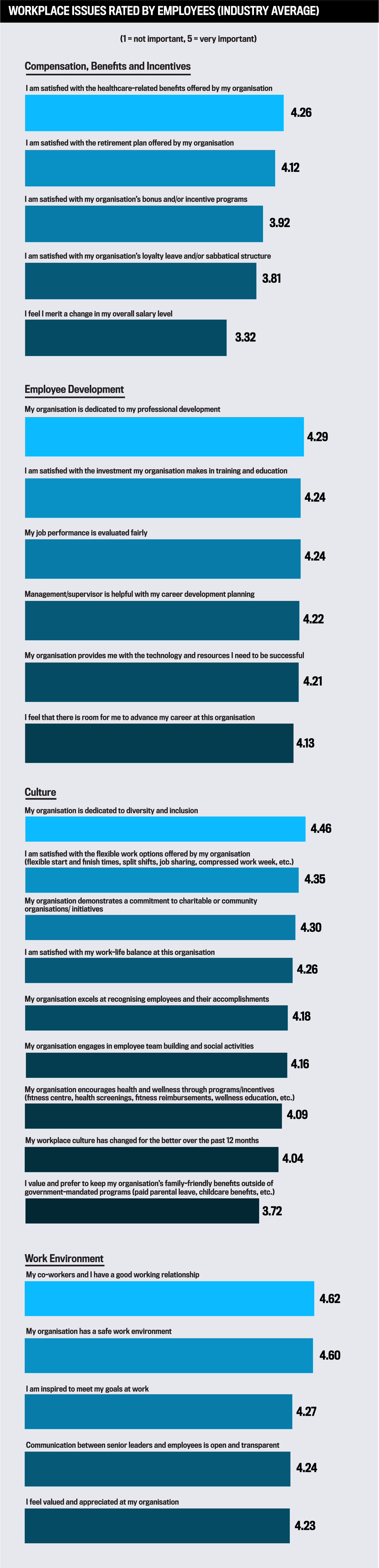

The box below shows IBUK’s survey results about what employees feel on a range of issues.

The key to remaining a Top Employer is to appreciate what these types of changes mean. “You’re getting new blood who want to do things differently, and they recognise that the voice of the employee is extremely important,” adds Gosrani.

These initiatives are in action at Arch. McLean says due to the diversity of the workforce it’s difficult to generalise, so they combat this with a thorough approach.

“We have established employee forums and multiple methods and process for capturing feedback and measuring employee satisfaction, from group-level surveys to individual sessions,” she says. “This feedback helps us to understand what staff want and implement suggestions that are beneficial to creating a positive and productive working environment. Our aim at Arch is to continue to build on the success of our programmes and platforms to ensure that we are constantly listening and responding to the needs of our employees.”

On the survey, anonymous participants were largely happy with the work environment at Arch. Some expressed a desire for slightly better transportation options, more career development, better IT, maternity, and DE&I programs.

Meanwhile, Cooper prefers to think of what they can do to make working at Flood Re better.

“It’s important to stay focused and committed to our DE&I journey and clearly set out our ambitions,” she says. “We need to continue to nurture and take care of our culture – in my opinion, culture needs constant attention, it’s not about periodic culture exercises. And then we must continue to seek employee feedback so we really understand what it’s like working at Flood Re and use this to direct our efforts.”

“It is imperative that we ensure that the integration of flexible working does not hinder the development of the individual employee” Marcella McLean, Arch International

501+ employees

Crawford & Company

RSA Insurance

Specialist Risk Group

101–500 employees

Policy Expert

QuestGates

Quotemetoday.co.uk

26–100 employees

Momentum Broker Solutions

The Plan Group

10–25 employees

All Medical Professionals t/as All Med Pro & Grow Insurance Partners

Sutcliffe & Co. Insurance Brokers

To find and recognise the best employers in the insurance industry, IBUK first invited organisations to participate by filling out an employer form, which asked companies to explain their various offerings and practices. Next, employees from nominated companies were asked to fill out an anonymous form evaluating their workplace on a number of metrics, including benefits, compensation, culture, employee development, and commitment to diversity and inclusion.

To be considered, each organisation had to reach a minimum number of employee responses based on overall size. Organisations that achieved a 75% or greater average satisfaction rating from employees were named Top Insurance Employers for 2023.

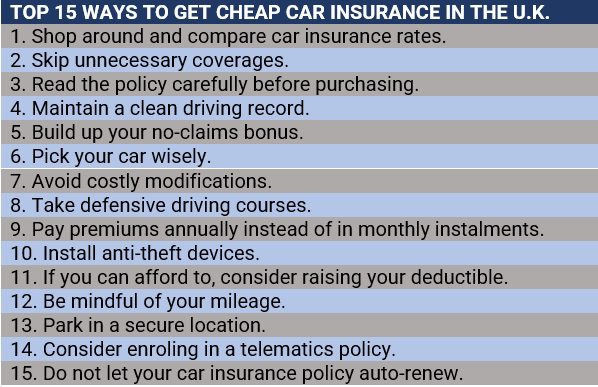

In this article, Insurance Business compiled a list of practical tips and strategies that can help British motorists save on car insurance premiums. Here are 15 of the most effective premium-reduction techniques that can help you land cheap car insurance in the UK. If you are an insurance professional with a client who is worried about the cost of car insurance, this is a good guide to help them.

1. Shop around and compare car insurance rates.

Because premium prices can vary significantly depending on a driver’s personal circumstances, determining which policies provide the greatest savings can prove to be challenging. A car insurance policy that offers the cheapest rates for you may be the most expensive option for another.

This is where price comparison websites can come in handy. The internet is replete with insurance comparison sites that you can easily access. These platforms allow you to shop around and compare quotes from several car insurance providers, which is often the simplest and most effective way to ensure that you are getting the lowest rates possible for the coverage that you need.

2. Skip unnecessary coverages.

Most car insurers offer a range of coverage options that can boost your policy’s protection level – but there’s a caveat. While the increased coverage these add-ons provide makes them very attractive features of your policy, they can also easily drive up the cost of premiums. So, it pays to be aware of the coverage you really need. Often, by sticking to the basics, you can also greatly lower your rates.

3. Read the policy carefully before purchasing.

To avoid overpaying, you should have a clear understanding of what you will be covered for and how much a plan will cost you. This is why it is important for you to carefully read through the policy document before purchasing. Doing so also enables you to get the right coverage at the best possible price. Be sure to double-check the quotes and if the coverage level suits your needs.

4. Maintain a clean driving history.

Keeping your driving record spotless is one of the best ways you can access cheap car insurance in the UK. If you are a safe driver, auto insurance companies often view you as more of an asset as you are less likely to be involved in vehicular accidents and, therefore, cheaper to insure. You may also be able to access a range of discounts for adopting safe driving practices like the one below.

5. Build up your no-claims bonus.

You can also significantly reduce the cost of your car insurance premiums by building up your no-claims bonus. If you have consecutive claim-free years, you may be able to take advantage of this type of discount. The amount can potentially rise each year, with some insurers offering up to 70% to even 80% reduction in premiums for drivers who have maintained their claims-free status for five straight years.

It can also help if you can make smart choices on what you claim. For example, paying for minor repair costs out of pocket if it means retaining your no-claims status.

6. Pick your car wisely.

The type of car you choose plays a huge part in how your premiums are calculated. Pricier vehicles are often more expensive to repair as they have parts that are difficult to replace, not to mention they are also more attractive to thieves, pushing up insurance costs.

In the UK, every vehicle on sale is categorised into a car insurance group, which helps insurers determine how much premiums they will charge. The groups are numbered anywhere from one to 50. As a general rule, the lower the insurance group, the cheaper it will be to have the car insured. We will delve deeper on how car insurance groups work later.

The right modifications can boost your car’s performance and make it more stylish – but these can also drive up premiums. So, if you want to cut down on insurance costs, you should carefully consider first if such enhancements are necessary. Another thing to take note of is that it is mandatory for you to declare any modifications done to your vehicle to your insurer, even if you were not responsible for these changes. Failure to do so risks voiding your coverage.

8. Take defensive driving courses.

Taking safe driving courses not only shows that you are committed to becoming a better driver, but also allows you to qualify for discounts. It would be best though to talk to your insurer before enrolling in courses to know which discounts you could be eligible for. An experienced insurance agent or broker can give you sound advice on the best route to take to qualify for lower rates.

9. Pay premiums annually instead of in monthly instalments.

Paying for your premiums in monthly instalments is like paying for a car loan – you are also likely being charged for interest or finance arrangement fees. If you can afford to, opt for annual payments. This can slash a substantial amount from your car insurance.

10. Install anti-theft devices.

Anti-theft devices play an essential role in boosting your car’s security – and car insurers like that. Most insurance companies will reward you with discounts if you have installed theft deterrents in your vehicle. These include:

Car alarms

Kill switches and immobilisers

Steering wheel locks

Brake locks

Locking wheel nuts

11. If you can afford to, consider raising your deductible.

A higher deductible means lower premiums. But this also increases the amount you need to pay before your car insurance picks the tab in the event of an accident or theft. Think carefully and make sure you choose a deductible amount that you can manage to pay. This strategy is not for everyone but if you are a safe and confident driver, you may be able to afford more risks.

One of the most common mistakes drivers make that prevents them from getting cheap car insurance in the UK is overestimating their mileage. For example, if you expect to cover 10,000 miles and declare this on your insurance policy, yet only drive 5,000 miles, you’re paying for a wasted 5,000 miles worth of insurance cover. It pays to be as accurate as possible when providing car insurance companies about how many miles you cover. But you shouldn’t be dishonest either as this can result in the rejection of your claims.

13. Park in a secure location.

A car left out on the street is always more vulnerable to theft, vandalism, and damage from careless drivers. This level of risk often leads to higher premiums. Conversely, if your vehicle is parked in a secure location, such as a garage, you can access cheaper rates. Keeping your car garaged also yields other benefits, including keeping your car looking pristine longer as it reduces damage caused by UV radiation, hail, and bird droppings.

14. Consider a telematics policy.

Enrolling in a telematics policy can be beneficial for certain types of drivers. This works with your insurer installing a telematics device in your vehicle. The device, also called a black box, tracks driving behaviour, allowing you to access discounts based on when, how well, and how much you drive.

15. Do not let your car insurance policy auto-renew.

One of the main reasons why many drivers choose to let their car insurance policies auto-renew is that they find the process of shopping around and applying for a new one arduous and time-consuming. But doing so can also make them miss out on a better deal.

According to experts, reviewing coverage and shopping around for a better deal is something that you should practice every year to reduce your premiums or find a policy that you’re happier with. By taking these steps, you can also determine if you’re still getting value from your current cover.

Here’s the summary of the top 15 ways to get cheap car insurance in the UK.

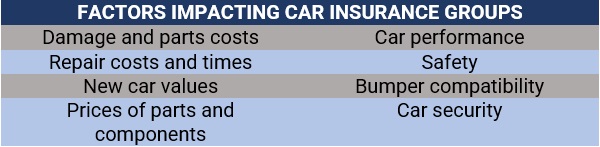

If you’re like most Brits, you probably do not pay too much attention to a vehicle’s insurance group before purchasing. This often-overlooked detail, however, has a major impact on your car insurance premiums.

As mentioned earlier, every vehicle on sale in the UK is categorised into a car insurance group, which helps car insurers in determining how much premiums they will charge. The groups are numbered anywhere from one to 50, with the cars falling into the lower insurance groups getting the cheapest rates.

A group rating panel consisting of representatives from the insurance industry and members of the Association of British Insurers (ABI) and Lloyd’s Market Association (LMA) are tasked to determine in which category each car will fall. To do this, the panel considers eight factors, with the goal of finding out how much damage a vehicle sustains in a collision and how cheap and easy it is to repair after an accident. These parameters are listed in the table below.

A vehicle’s insurance group, however, is not the only factor that car insurers take into account when calculating coverage costs. Insurance companies also consider several parameters, including:

Age: Young and inexperienced drivers are often considered riskier to insure and face higher premiums than their older counterparts. Parents who are thinking about adding their teenage children to their policies should also be aware that doing so can drive up premiums depending on their kids’ driving history.

Driving record and claims history: Past accidents and claims increase a driver’s risk, which leads to higher premiums. Motorists with a clean driving and claims history, meanwhile, are often rewarded with discounts from their insurance providers.

Residence: Car insurance rates for postcodes with higher vehicular crime and accident rates will likely be higher.

Level of coverage: The choice of policy also dictates how much a driver will pay in car insurance.

Vehicle’s market value: A car’s age, make, model, condition, and distance travelled also play key roles in calculating premiums. Ever wondered if newer cars are more expensive to insure than older ones? Find out in our new car versus old car comparison.

Parking location: Keeping a vehicle in a secured garage or monitored car park will likely result in cheaper premiums compared to just leaving it on a public road.

Add-ons: Adding optional extras such as roadside assistance, widescreen excess, and rental car cover can raise premiums, although some comprehensive policies already offer these types of coverage.

It is mandatory in the UK for drivers to take out third-party coverage. Getting caught driving without one can result in hefty penalties and may affect your future eligibility for obtaining coverage. Auto insurance, however, goes beyond just liability coverage.

UK drivers can access three types of protection, according to the ABI. These are:

Third-party coverage: The most basic form of cover, this pays out for injuries or damage you caused other people, properties, and vehicles. This is also the minimum level of cover required for you to be allowed on the road.

Third party, fire, and theft (TPFT) coverage: This provides the same protection as third-party policies but also covers if your car is stolen or if it catches fire. Some auto insurance providers also require that the vehicles have a security device installed for theft coverage to kick in.

Comprehensive coverage: This offers the most extensive coverage available. Apart from third party, fire, and theft, comprehensive policies cover the cost of repairing your vehicle after an accident even if you are at fault.

Car insurance is one of the biggest costs associated with owning and operating a vehicle. In the UK – where there are more than 40.8 million registered vehicles, according to the latest vehicle licensing statistics from GOV.UK – drivers are legally bound to carry at least one type of coverage – third-party insurance. But with motorists swamped with options from various providers, finding the right policies that fit your needs becomes a challenging task.

Choosing cheap car insurance in the UK can often be tempting. But you risk losing more, especially if the protection such policies provide is not enough. To get the most out of your car insurance, you must first understand the choices available to you and the level of coverage the different types of policies offer.

For families looking for cheap car insurance, they can check out our latest rankings of the cheapest family cars to insure in the UK. Sometimes, the best way to get cheap car insurance is to start with the actual car that you purchase and then go from there.

Do you think cheap car insurance in the UK provides sufficient coverage? Tell us why or why not in the comment section below.

In this #IBTalk episode, H&H Insurance Brokers’ MD Paul Graham shares insights into how insurance brokers can move the dial on how insurance is viewed by customers.

UK holidays group and insurer Saga Plc (Saga) is in exclusive discussions with Australian insurance group Open Insurance (Open) regarding a potential sale of the UK insurance business’s underwriting arm, Acromas Insurance Co., according to reports.

Acromas currently underwrites around 25% to 30% of the insurance business, making it the largest business in the group. However, it has struggled due to rising claims, leading to a half-year loss and a threat to full-year earnings in September. As of July 31, 2022, the company’s net debt was £721.3 million.

In a statement, Saga said it was “committed to providing a best-in-class insurance offer to its customers” and was looking for ways to “optimise [its] operational and strategic position in the insurance market, in line with the evolution to a capital-light business model and the stated objective to reduce debt.”

It added: “[The board] has concluded that a potential disposal of its underwriting business is consistent with group strategy and would crystalise value and enhance long-term returns for shareholders.”

We use cookies to ensure that we give you the best experience on our website. If you continue we will assume that you are happy with it.AcceptPrivacy Policy

Kieran Boyle, CKB Recruitment

Kieran Boyle, CKB Recruitment

Jo Morgan, TH March

Jo Morgan, TH March  Jenny Cooper, Flood Re

Jenny Cooper, Flood Re

Marcella McLean, Arch International

Marcella McLean, Arch International