Intangic MGA said in a press release that the CyFi product is meant to complement and strengthen existing cyber indemnity cover, not replace it. The product also does not have a claims adjustment, and in the case of a material breach, policyholders can expect a fast payout in days as opposed to months.

“A high-frequency risk”

Intangic MGA has analysed thousands of corporations over several years, and in the process found that companies struggling to manage the financial impact of cyberattacks have a 250% higher probability of suffering material losses than peers who had better cyberattack management. This new cyber parametric policy is designed to address the problem of constant cyberattacks as early as possible to lower the probability of customers suffering losses from attacks.

Intangic MGA founder and CEO Ryan Dodd (pictured above) attributes this to a difference in thinking about the problem.

“The security teams at large corporations have to manage cyber threats all day, every day. Our approach assesses cyber as a high-frequency risk. By accepting cyber attacks as ‘constant’, we can measure a link between how these attacks are managed and the financial impact they have on corporate operations,” he said.

According to Dodd, CyFi’s parametric triggers make this link visible, enabling fast recovery from covered material breaches. He also said the product has converted cyber risk to a language that the board of any company can understand.

AXA XL UK and Lloyd’s chief underwriting officer Luis Prato said that CyFi represents a simple solution to a complex problem.

“Intangic’s policy and the mechanisms behind it create a different way to approach risk and unlock capacity for cyber for large public corporations, helping them to strengthen their cyber risk programme,” he said.

In this article, Insurance Business sheds the light on common queries you may have about life insurance in the UK. Questions such as “What is life insurance?” and “What are the types of policies available?” are among those that we will provide answers to. For the mortgage professionals who make up our core audience, this article could serve as a good reference for any clients of yours who have questions about how life insurance in the UK works.

Just like in other countries, life insurance plans in the UK provide a lump-sum payment to the beneficiaries either at the time of the policyholder’s death or after a set period. This financial benefit has made life insurance one of the most popular forms of coverage in the UK.

Your life insurance policy will remain in-force for as long as you meet your premium payments on time. Depending on the type of plan you choose, your coverage can end after a set term or last a lifetime.

You can likewise pick between two types of cover:

1. Single life insurance policy

This type of life insurance plan covers only one person and pays out the death benefit if they die during the length of the policy, at which point coverage ends. Some couples opt to take out separate policies, so they will still have coverage even after their spouse or partner dies.

Single life insurance benefits are also paid into your estate, allowing you to choose your beneficiaries. We will discuss life insurance beneficiaries in detail later.

2. Joint life insurance policy

A joint policy covers two lives, but only pays out after one person dies, after which coverage ends. The death benefit goes to the surviving partner, unless other arrangements were made.

If a couple with a joint life insurance plan separates, they may be able to convert this into two single life insurance policies.

Insurers offer different types of policies, with each offering varying levels of financial protection. In general, life insurance plans in the UK come in two major categories. These are:

1. Term life insurance

As the name suggests, term life insurance policies run for a fixed term. You are free to choose the coverage amount and policy length but bear in mind that your choices have a corresponding impact on premiums. Term life insurance pays out a benefit only if you die within the set timeframe. Otherwise, the insurer keeps all the premiums you paid. Some providers, however, also cover you if you become terminally ill.

If you’re considering taking out term life insurance, there are three types of plans you can choose from. These are:

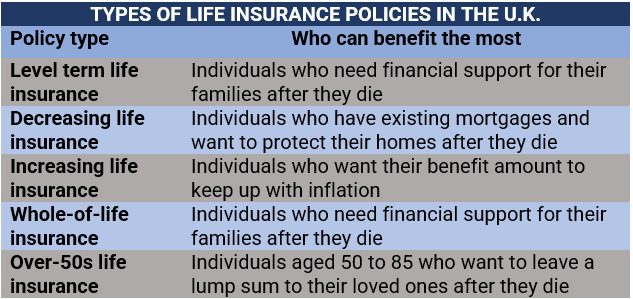

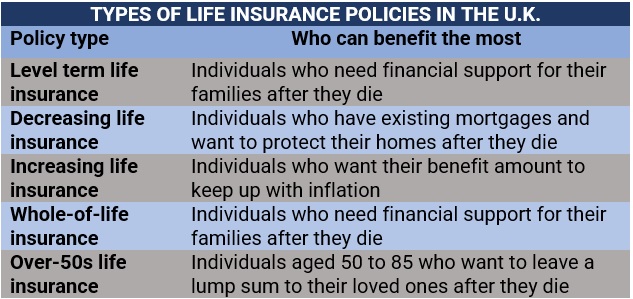

Level term life insurance: Or simply life insurance, pays out a lump sum if you pass away within the agreed term, with the level of cover remaining the same throughout.

Decreasing term life insurance: This type of policy is often used to pay off your mortgage, that’s why it is sometimes called mortgage protection insurance. The death benefit amount reduces each year to correspond with your loan balance, although your premiums remain the same.

Increasing term life insurance: The death benefit amount in this type of policy increases throughout the plan’s term to keep up with inflation.

2. Whole-of-life insurance

Whole-of-life insurance, also called a life assurance plan, provides lifetime coverage, with the payouts given to your beneficiaries after you pass away. Because of the level of coverage this policy provides, the premiums are also more expensive compared to those of term life plans. One major drawback is that if you live longer than expected, you may end up paying more than what you can get out of the policy.

And just like whole life insurance in the US and Canada, this type of life insurance in the UK sometimes includes an investment element that you can access while you’re still alive and can be sold through financial advisers.

Term life insurance. Whole-of-life insurance. These are just some of the buzzwords you’ll encounter when taking out life insurance in the UK. If you want to know the meaning behind the different life insurance jargon, our glossary of common insurance terms can help.

Over-50s life plan

Not considered a major category, some UK life insurers offer over-50s life plans, which provide coverage for individuals between 50 and 85-years old. Premiums are based on the benefit amount and the policyholder’s age. These plans also offer guaranteed acceptance, meaning applicants are not required to submit medical information. Because of this, rates are often higher as insurers have no way to predict the plan holder’s risk level.

Over-50 plans’ are typically capped at around £20,000. There is also a waiting period that can range from 12 to 24 months. If the policyholder dies due to natural causes within this period, the beneficiaries will not receive a benefit but the premiums they paid will be returned.

Who needs life insurance?

While not everyone may need this form of coverage, there are certain types of individuals and groups who can benefit the most from taking out life insurance. They include:

Breadwinners

Parents of school-aged children

Parents who have dependants with special needs

Families with existing mortgages

On the other end of the spectrum are individuals who do not need life insurance, including:

Singles

Those whose spouse or partner earns enough for their family to maintain their lifestyle

Low-income earners who can qualify for state benefits

Some employers also offer employee packages that include death-in-service benefits – which work somewhat similar to life insurance – with a coverage amount linked to your salary. That’s why it pays to check with your company to see if you already have cover. However, you may still need to take out a life insurance policy if you feel that the benefits you are eligible for are not enough to sustain your family’s lifestyle after you die.

Another thing to remember is that employee packages are non-transferrable. This means that when you leave your employer, you cannot take the benefits with you.

The table below sums up the different types of life insurance in the UK and who can benefit the most from each.

A pre-existing condition does not necessarily prevent you from taking out life insurance in the UK but there are some additional factors you need to consider. These include:

The insurance company may require additional medical information: Insurers may require you to undergo further screening and medical examinations to learn more about your condition. Some providers cover the cost of these tests.

Your premiums may cost more: If you get approved, your insurer may charge higher premiums, depending on the severity of your condition, as you also present a higher risk.

Another option is an over-50s plan, which offers guaranteed acceptance. These plans, however, do not provide the same level of coverage as standard life insurance policies and can even cost higher.

During the application process, your insurer will ask you several lifestyle- and health-related questions to determine your risk level. It is very important for you to answer these questions accurately and honestly, and to disclose any pre-existing medical condition.

Your insurance provider regularly checks the medical information you provided and may contact your doctor for confirmation. If you have been found to deliberately withhold important medical details from your insurer, they may cancel your policy and void coverage.

As the policyholder, you can name anyone as a beneficiary of your life insurance plan. These include:

You can also name the beneficiaries as an individual or group. If you have a single life insurance plan, the benefits will be paid into your estate, where the beneficiaries are named through your will. If you do not leave a will, the proceeds of the estate will be shared according to the rules of intestacy.

You can likewise name beneficiaries when you place your life insurance in a trust. Doing so has potential benefits, including:

The benefits will not be counted as part of your taxable estate, meaning the lump sum will be passed on to your beneficiaries exempt from Inheritance Tax (IHT).

The benefits can reach the beneficiaries faster if there are appointed trustees who will take care of the process after you die.

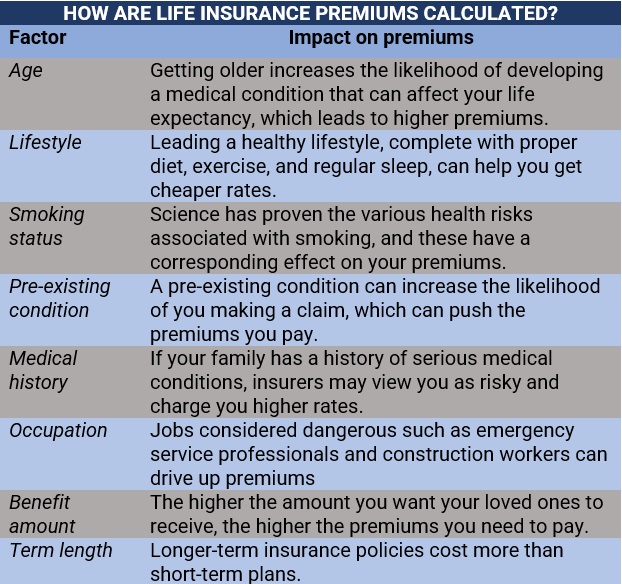

Because each person’s lifestyle and health status vary significantly, it’s difficult to provide a ballpark figure to represent the cost of standard life insurance in the UK. Premiums are influenced by a range of factors. The table below sums up these parameters and how they impact life insurance rates.

The answer to this question depends on your personal situation. If you have people who are heavily reliant on you financially, then life insurance can help provide some level of monetary support after you die. Taking out life insurance can also help pay off your mortgage if your beneficiaries do not have the financial capacity to do so.

Not everyone, though, needs this type of coverage. If your wealth is enough to maintain your loved ones’ lifestyle after you pass away, then purchasing life insurance is unnecessary. It’s the same if you are single with no dependents.

If you want to know how life insurance policies work in different countries, you can check out our global life insurance primer.

An experienced insurance agent or broker can give you a rundown of the types of coverage that best fits your personal circumstances. We recommend that you check out our Best Insurance for UK page to find reliable and trustworthy insurance professionals near you.

The insurance companies featured on this page are nominated by their peers and vetted by our team of experts as reliable leaders in the industry. By dealing with these providers, you’ll have the peace of mind of knowing you’re getting the best coverage from someone who can be trusted during difficult times.

Are you searching for the right life insurance plan? Which features and benefits do you think are important? Share your thoughts in the comments section below.

UK chartered insurance broker Verlingue has announced the hiring of Jon Bethell as its head of private clients. The appointment is part of the broker’s plans to rapidly expand and grow its existing high-net-worth (HNW) offering.

In this new role, Bethell will use his specialist expertise to develop a market-leading HNW proposition at Verlingue, as well as delivering new growth and development opportunities.

“A real asset to Verlingue”

“Jon is a real asset to Verlingue as we look to build out our existing private clients business. He has over a decade of experience in this sector and already has very strong relationships with many of our key insurer partners. His experience of building high performing insurance teams based across multiple locations will also ensure we can deliver on our ambitious growth targets in this sector,” Verlingue CEO Mike Latham said.

Bethall has two decade’s worth of insurance experience. His most recent posting before the UK broker was with insurer Hiscox, where he worked for 12 years in supporting some of the country’s largest brokers. He last managed the trading team at Hiscox. Before that, his roles included claims and underwriting functions at Ageas and Aviva, respectively.

The firm also recently created a dedicated media practice, headed by client director Maia Olesen – a move corresponding with plans to expand Verlingue’s presence in the fast-growing independent media sector.

What are your thoughts on this story? Please feel free to share your comments below.

Through this new capacity, Coalition is set to help more businesses get the coverage that they need in order to better protect themselves from digital risk. The insurer will extend its reach to provide full-follow form coverage and protection of up to £10 million above a primary layer of insurance from another insurer for both cyber and technology professional indemnity (PI) lines.

Greater reassurance with state-of-the-art prevention technology

“Our new excess product is designed to help UK brokers struggling to find enough cyber and tech PI protection for their clients. By bringing in Coalition to provide excess cover, brokers give their clients greater reassurance with our state-of-the-art prevention technology and early threat warnings from our 24/7 internet scanning operation,” said Tom Draper, UK head of insurance for Coalition.

The excess policy from Coalition provides the added benefits for policyholders of access to Coalition Control, the insurer’s proprietary attack surface monitoring technology that delivers personalized risk assessments, in addition to advice from Coalition’s in-house incident response cyber support team. Allianz and Lloyd’s of London will support Coalition’s policies.

Coalition also offers excess of loss cyber products in the US and Canada. Interested brokers can submit directly to Coalition’s underwriting team and find out more through the official site.

Insurance telematics solutions provider Trakm8 has commissioned a new national driver survey that revealed some insights on the cost of living, technology, and other factors that impact how drivers purchase insurance.

The survey found that 69% of UK drivers expect to drive more miles in 2023 than last year. Seven out of 10 (70%) of them also expect their mileage to be higher than pre-pandemic levels. Additionally, more than half (58%) of the survey’s respondents said that they are considering a telematics insurance policy to reduce costs associated with car usage and mileage increase.

Survey results are “fairly surprising”

The survey yielded some “fairly surprising” results, Trakm8 insurance managing director Adam Gooch said, as it did not align with the expectation that the rising cost of living would “impact the number of insured vehicles on the road and total mileage expected to rise in 2023.” Additional information from the survey showed that very few households in the UK – equivalent to 9% – will be reducing the number of insured cars due to the cost of living.

Trakm8 collaborates with some of the country’s leading insurers as a provider of telematics policies. The firm’s end-to-end solution includes a portal that provides instant driver and vehicle insights such as journey information, driver scoring/alerts and vehicle health, as well as an app that gives drivers an easy-to-use interface with an overview of their driver data and scoring.

“It is really positive to see so many more drivers receptive to a telematics policy to reduce costs and reward good driving. Our comprehensive end-to-end insurance telematics solutions are designed to give insurers a unique opportunity to help personalise policies based on a customer’s habits and requirements,” Gooch said.

What are your thoughts on this story? Please feel free to share your comments below.

The schemes market is full of highly lucrative opportunities and brokers all over the world want to get in on the action.

Join Simon Medhurst for a deep dive into the schemes market and the value of brokers getting involved. Learn how to provide exceptional value tailored to your clients’ needs, the advantage of a partnership-first approach and a robust framework, and how Travelers 4D (discovery, design, delivery & development) process works to create a great scheme.

By the end, you’ll understand the secret recipe for a successful scheme and how brokers can harness these exclusive opportunities.

Understanding the schemes market has never been easier. Don’t miss this informative podcast and everything it has to offer on the schemes market.

Clients and partners should expect a “more consistent underwriting approach”, with coordination on global scale, the insurer said.

“Allianz Commercial allows us to deliver the full value of Allianz’s scale and full set of capabilities for the benefit of our customers, brokers and shareholders,” said Chris Townsend, member of the Allianz SE board of management.

Allianz Commercial will feature one single lead in each country or region to represent its commercial businesses, a move it said is intended to simplify the experience of clients and distribution partners.

Its trading, underwriting, and customer delivery teams are expected to “work closely together” under the model, according to the press release. The legal entities conducting the insurance business and their leadership are expected to remain the same, Allianz said.

Restructuring its leadership and management team

ACGS has added two new members to its board of management while also updating the responsibilities of existing members.

Joachim Mueller will now lead the Allianz Commercial business as part of his role as CEO of AGCS SE, reporting to Townsend.

Jon-Paul Jones will assume the role as chief operating officer of AGCS, pending regulatory approval, replacing Betting Dietsche, who has already moved to Allianz SE as chief people and culture officer. Additionally, since February 1, Dirk Vogler has been working as the midcorp transformation officer.

Jones will oversee global business operations, IT, protection and resilience, corporate service transformation, global process management, the global data office and major IT transformation projects.

Vogler oversees the program office, which was also created to support the new collaborative model between AGCS and the mid corporate business of national Allianz OEs.

Other notable transitions

Besides these two appointments, various changes in responsibility have come into effect for current AGCS SE Board Members:

Chief underwriting officer specialty, Renate Strasser, will move to a newly-created AGCS SE board role as chief technical officer, overseeing all global functions that focus on technical excellence in underwriting, pricing, portfolio management, risk consulting and reinsurance, as well as ESG/climate solutions.

Shanil Williams will now take on greater responsibility for all nine AGCS global lines of business, both corporate and specialty, as chief underwriting officer.

Claire-Marie Coste-Lepoutre will head the compliance, human resources and the ‘NEW AGCS’ transformation program office. She is also the new deputy CEO on the AGCS SE board, replacing Mueller.

Alongside his role as CEO of AGCS SE, Mueller will also take responsibility for business in the United Kingdom, France and Australia. Each country has large Allianz MidCorp portfolios and are key parts of the integrated commercial AGCS/OE partnership.

Other countries or regions will continue to report to either Henning Haagen, chief regions & markets officer 1, or Tracy Ryan, newly appointed as chief regions &, markets officer 2.

“I welcome Dirk and Jon-Paul to AGCS as new members to AGCS SE Board of Management, in addition to Tracy Ryan whose appointment we announced a few days ago” Mueller said. “With these new joiners and a new allocation of responsibilities for some current board members, we, as a leadership team, are ready to open the next chapter in AGCS’s corporate history: the realisation of the new collaborative model of Allianz Commercial.”

“When I reflect on what’s changed, I think, really, there are three things,” she said. ”The first thing is that our customers and clients demand something different from us as an industry. And people want to interact with us, how they interact with other things in their lives – whether it’s buying stuff online, or whether it’s communicating with their bank. So, I think there is a push from our customers.”

The second major change is that internal organisations across the insurance ecosystem appear to now have a greater willingness to adapt to technological change, Ladva said. She identified how quickly the industry shifted to online meetings during COVID as an example. Previously, that scale of change would have taken six months of training and workshops, etc. but almost overnight, entire workforces moved online – reflecting the lower barrier to entry and reduced resistance to technological change within organisations.

“And finally,” she said, “I think the things that technology can do now have changed. I think all those three things in the last five years have made a difference. But we haven’t quite caught up yet…. And to catch up, I would say we really need to focus and we need to execute. I think our Achilles heel as an industry is our ability to get stuff done and get stuff done quickly.”

How can insurance accelerate into the next generation?

During Ladva’s keynote address, host Louise Smith, chair of the UK board of the global financial services software firm Stripe, identified how the rest of the financial services sector generally views insurance as behind the technology curve, albeit with the ability to outstrip them in the future. But what are the barriers preventing insurance from making that leap? And what transitions will be required to accelerate insurance into the next generation?

For Ladva, the answer really comes down to having a “relentless focus on the customer or the client.” Different stakeholders across insurance will define that in very different ways, she said, but the industry is primed to overcome that barrier due to the bright, clever and incredibly forward-thinking individuals that make up the sector. She emphasised, however, how important it is for the insurance sector to celebrate its inherent creativity as well as its strong data and tech proficiencies.

People outside of the insurance industry don’t seem to recognise that creativity, she said, but it’s, “a fascinating part of what we do.” So, insurance should look to utilise and amplify that creativity to truly ensure that the customer is at the heart of everything it does and all the solutions it creates.

“Secondly,” she said, “I think the other barrier and challenge that we face – and it’s not unique to us, but I think it has a greater challenge for us – is talent. Everybody in the world is after the same talent.”

How can insurance access the best talent?

Another company with a bigger brand name which is operating in a different industry probably has an easier time attracting great talent, Ladva said, and so the question for the insurance market is how can it encourage the best people to join the sector. And the answer starts with understanding why individuals are not currently attracted to the insurance market which goes back to importance of advertising the creativity to be found in insurance – but it’s also about finding creative solutions to plug that talent gap.

“The way I think about solving that is that first of all you have to look at who you already have,” she said. “Think about how do you repurpose, how do you retrain, and how do you create a real learning culture?… I think that’s the first thing. And then the second thing is how do we make what we do in insurance attractive for people to want to come and join us?

“And there, the thing I’ve realised is purpose. We have a real purpose in what we do in this industry. We talk about making the world more resilient but what does that actually mean? So when you explain to younger talent about how by using satellite imagery, you can predict supply chain risks they’re like, ‘really? Is that what you can do?’ So, it’s about creating a purpose out of our industry which attracts talent that sometimes would go elsewhere. I think those things are probably, as well as a focus for execution, things that concern me.”

What are your thoughts on the pace of innovation in insurance? Please feel free to share your comments below.

Specialty managing general agent (MGA) Optio Group has named Tom Kennett as its UK head of political violence and terrorism (PVT). Kennett will be based in London and will report to PVT global head Chris Kirby.

Kennett brings with him both broking and underwriting experience, with 12 years of class-specific expertise. His most recent posting was with Munich Re Syndicate, where he held the role of senior PVT underwriter. Before this, he held a number of senior positions, including PVT senior broker at both Aon and Marsh, where he focused on building a global partner network and sourcing new business opportunities within emerging markets.

“The last few years have been the most active on record for the global PVT market and we have been bolstering our presence and product offering to support this growing segment,” Kirby said. “Tom’s market standing and experience, as well as his impressive background in business production both through the London market and international brokers, will be essential as we continue to realise our ambitions across North America and Western Europe. His global outlook and underwriting approach complement our own and I very much look forward to working with him and welcoming him to the team.”

Kennett’s appointment comes at the heels of Optio Group naming its new CEO a few weeks ago, with David Robinson moving into the role.

What are your thoughts on this story? Please feel free to share your comments below.

That said, both groups agree on the percentage of people who may experience a negative impact with hybrid work, with employers listing 6% and employees listing 7%. Both groups acknowledged that hybrid work is not a positive experience for everyone in the workspace.

GRiD noted in their study the importance of recognising that although a relatively small percentage of people overall view hybrid work as a negative impact in their careers, it still represents a large number of employees. The industry body stressed that while many people feel that a flexibility in working locations is beneficial, it’s important that employers don’t assume or change their workplaces or working practises in a way that could potentially harm their workforce.

“A slightly exaggerated view”

“Employers have a slightly exaggerated view of just how much hybrid working is benefiting the health and wellbeing of their staff. It’s clearly the case that many do find it a positive experience but employers should be careful not to assume this is a panacea for everyone. It’s important to note that health and wellbeing support will still be required for everyone, and particularly for those who have found the change in working patterns more difficult to cope with,” GRiD spokesperson Katharine Moxham said.

The study found that mental wellbeing was the area that employees felt was most improved for those who felt hybrid work’s positive effect, with 68% of respondents agreeing. This was followed by social wellbeing at 45%, financial wellbeing at 44%, and physical wellbeing at 43%.

The research noted that despite mental health being the largest beneficiary of hybrid working, in addition to reduced costs of commuting associated with financial health, it is of interest that social and physical benefits were reported by employees, too.

“Employers may have already seen the benefits to physical and social health by allowing staff to relinquish their journey to work, allowing employees to spend more time with family and friends and potentially using the time for fitness activities to improve their physical health,” Moxham said.

The research found that half of employees said they have a choice about whether to work from the office or at home, a figure which largely tallies with statistics reported by employers. Of employers surveyed, 22% said that they have given all their employees a choice about where they work from, and 34% said that they have allowed some but not all of their employees to make the same decision.

Despite the results tilting heavily in favour of its positive effects, employers must not consider hybrid work to be a benefit in and of itself. GRiD stated in its study that hybrid work is not a replacement for a comprehensive program of benefits to support health and wellbeing such as private medical insurance or group risk benefits including employer-sponsored life assurance, income protection, and critical illness.

It’s important to have a full suite of support available for when an employee struggles with a health or wellbeing issue. While working from home may help some, it’s not always suitable for all, and the report noted that it is not a fix when more serious issues come to light.

“Employers who fully support the health and wellbeing of their staff through a programme of employee benefits and other flexible policies, will be rewarded with a more engaged and more proactive workforce. Hybrid working can play a role but it’s not the silver bullet,” Moxham said.

What are your thoughts on this story? Please feel free to share your comments below.